At the end of my last post I stated I wanted to cover the,

…banking system and how it will exacerbate the shock to the financial system when whatever sovereign does what it’s going to do. Specifically, I’ll expound on liquidity. How it works and why every pro in the world already knows the danger it presents when it dries up.

For an outstanding and general explanation of liquidity within a market system, have a read of the excellent March 2015 piece, Liquidity, by Howard Marks. He shares simple but keen insights on liquidity’s functionality across the entire financial market eco-system. The masters always make the difficult seem simple.

The liquidity I’ll be referring to is really more akin to leverage and it’s how a significant percentage of the party is funded in the investment world between banks, asset managers, pension funds, insurance companies, corporations, hedge funds, and various other entities.

Let’s start with what I suspect to be the average opinion of how a financial layperson thinks the system works.

The financial layperson thinks the investment world takes in cash and assets from clients or customers and then redirects those resources into investments for the benefit of everyone involved. On the surface, it is that simple. Bank takes in customer deposit, then lends out cash at a premium. Asset manager takes in customer investment capital, redeploys into assets with an expected ROI.

But for those in the know, there’s a much more sophisticated game played behind that simple perception. The game of lending and insurance but under a different name called derivatives, specifically swaps and repos. Observe how the financial world actually works, courtesy of the Office of Financial Research.

Even if you don’t understand all the components or every aspect of the diagram, the complexity and interconnectivity should jump right out at you. “Securities Dealers” and “Broker-Dealers” are essentially just banks. Major banks. Systemically important banks.

Even if you don’t understand all the components or every aspect of the diagram, the complexity and interconnectivity should jump right out at you. “Securities Dealers” and “Broker-Dealers” are essentially just banks. Major banks. Systemically important banks.

What this diagram maps out is how the financial system constantly redeploys other people’s money (“OPM”) to eke out additional yield or lever up on a “winning” thesis. This system diagramed above is the direct result of rocket scientists, PhDs, and all other people too smart by half taking their game to Wall St. instead of sharing their talents with the world of science.

That too is a direct result of too much money and glory heaped upon the successful investment managers in the the last four decades. But all the low-hanging fruit has been picked and what we’re currently left with is an investment ecosystem fraught with risk, overloaded with high IQs, and very little excess returns on investment.

A very significant percentage of the asset classes flowing through the diagram up above are interest rate swaps and credit derivatives. Major institutions think they can outsmart the sovereign entities of the world by hedging against the interest rate risk created by the central banks of the world. So trillions of dollars are traded in interest rate swaps, which in turn can be funded via a repo transaction. Do you see how the complexity of the financial system’s plumbing increases total system risk?

What’s a swap? What’s a repo? Well they don’t involve spouses or cars, sluggo.

Remember, they’re typically utilized as a hedge and very often just an outright speculation. One of the terms I love that banking pros use in place of hedge is “immunization overlay.” Really? I need an immunization overlay to protect my bet on the 3 ponies in the 5th race for the trifecta. Only bankers. Anyways…

A swap is a “simple” transaction between two parties. There is a multitude of various types of swap transactions but significant percentage of swaps are used for interest rate derivatives. As an unrealistic but clean example, let’s say Entity A owns $50 million in Deutsche Bahn 5-year bonds yielding whatever and Entity B owns $50 million in floating-rate notes from the US Treasury yielding who cares.

Let’s say Entity A is worried that the Fed Funds rate will somehow affect the value of its fixed rate bond from the German Railway company, and they know Entity B has some floaters that will create a potentially more profitable use of their money in light of their thesis. Entity B has the opposite stance and thinks volatility in Fed Funds rate will negatively affect the value of their floaters and they think a steady-eddy holding in Deustche Bahn debt in euros may be a better allocation of capital. The two entities can simply swap the cash flows of each of the debt instruments and voila! Asset quality is altered and risk is hedged.

Did you see how simple that was? Reality is never that simple.

Now here’s where the game get’s even more interesting. Entity A believes so strongly in its thesis that it thinks it can use its German Railway debt to speculate a little more. Entity A calls up Bank X and says it has $50M in Deutsche Bahn 5-year bonds and wants some cash to speculate against US entities sensitive to movements in the Fed Funds rate. Bank X says ok and it’ll give Entity A $45M for the DBahn bonds which Bank X will hold as collateral for 90 days. At the end of the 90 days, Entity A has to repurchase (“repo”) the Railway bonds from Bank X at the full $50M. That $5M difference between the cash amount and the repo amount is called the “haircut” and it’s a gigantic source of cash flows for the banking system. Everybody wins! Right?

Technically, this repo example is just a collateralized loan, and repo is often utilized in government securities as opposed to private sector assets. None the less, a repurchase agreement is a repurchase agreement.

Entity A can now go short the companies sensitive to US interest rates. Bank X gets a cool $5M for lending out other peoples’ money. Observe a simple diagram of a repo transaction below.

There’s another kicker for Bank X, as now it has those Deustche Bahn bonds on it’s balance sheet but maybe it doesn’t want them. So Bank X finds another entity willing to take those bonds in another repo transaction but only for 60-days, so that it may use the cash generated to go speculate in some other asset class.

There’s another kicker for Bank X, as now it has those Deustche Bahn bonds on it’s balance sheet but maybe it doesn’t want them. So Bank X finds another entity willing to take those bonds in another repo transaction but only for 60-days, so that it may use the cash generated to go speculate in some other asset class.

Let’s say instead that Bank X does nothing but holds onto the DBahn bonds as collateral. In the event that Entity A runs into financial troubles and depending on how the contracts of the transaction were worded, then Bank X can liquidate those bonds when and where they see fit in order to be made whole if it looks like Entity A is in trouble.

These kinds of transactions are the lifeblood of the financial system. This is how the banks, hedge funds, asset management shops, etc., find liquidity to speculate in whatever endeavor in need of cash flow. You might know this system under another guise, shadow banking.

This is precisely how the 2008 crisis was exacerbated. There were trillions of dollars of these sorts of transactions in the mortgage backed security (“MBS”) arena. Unfortunately, the whole system is based on confidence. Each of the players believe in and have confidence in the stability of the system and the valuations of the assets classes in which they are playing as well as the valuation and credit worthiness of the other players. We all know what happens when confidence leaves the station.

The central banks of the world think they have risk managed within the financial system via their controls, regulations, and ability to manipulate the money supply as well as interest rates. Here’s their perception of a ring-fenced system.

But literally every pro and every central banker knows this pic to the right is a joke. And a cruel one at that.

Everyone knows that there is literally no stability once confidence decides to jump out of a window. When players in the financial system lose confidence in the financial system due to the sheer amount of debt in existence at the sovereign level in combination with the incompetent monetary policies already in existence, it’s going to be a fire sale. Everything will go in the most indiscriminate manner which will only fuel the fire. Every single banker, professional investor, PhD economist, and educated corporate executive knows this. But you aren’t going to see reports about this on MSNBC or the front page of the Times.

Here’s the reality of the interconnectivity of risks within the financial system. The risks are shared throughout the system.

It’s one giant, incestuous orgy to share cash flows and risks and it can’t be stopped. The only way this game stops is via a crash and a reset of the financial system. New laws. New regulations. New players.

The rules change but the game is the same. Why do you think all these quotes stand the test of time?

Securitization was dreamed up as an innovation to hedge risk tied to debt. Unfortunately, all the incredible amount of debt and innovation have achieved is to gum up the financial system and turn liquidity(smooth oil) into a viscous sludge when it disappears along with confidence.

Care for a better diagram than the previous. Take Deustche Bank. It has the highest derivative exposure of any major bank in the world. It’s easily in the worst financial position amongst all the largest banks in the western world.

It’s financial connectivity just might be enough to spark a chain reaction if Deustche Bank fails. As I stated in my previous post, I think it’s a sovereign nation that ends the music for the next crash. But that doesn’t mean that bank failures aren’t on the program.

A majority of these swaps, repos, and other derivative transaction are done bilaterally; meaning just between the two parties. Central banks would love for all these kinds of transactions to go through a third party to clear these transactions and the third party be obligated to report the transactions. Makes sense, right?

But there are no laws forcing the use of a central-clearing, third-party. And in the financial system, entities are always going to act for their benefit. A majority of these transactions provide a superior benefit via bilateral facilitation.

Don’t think for one second that the risks associated with current worldwide debt levels and the transactions I just described up above aren’t entirely real. Why do you think the Fed makes the major banks conduct a stress test under an “adverse” scenario? Have a look, courtesy of JPM, at the very plausible scenario below that the Fed ensures each major Wall St. bank will be able to “survive” at current capital levels.

Unemployment jumps to 10%. House prices fall by 25%. Equity markets tank by half. I’d say this is a very real scenario. What’s totally fiction is the safety of the banks based on their capital levels in the event that a crash creates the stated conditions.

These stress tests are called the Dodd-Frank Stress Tests (“DFAST”). There’s nothing stressful about these stress tests for the banks, as DFAST is a farcical play put on for the masses to make it seem as if the banking system is properly capitalized.

It’s not. That’ll be proven again. In spades.

The DFAST is a well-intentioned undertaking that even makes the banks detail the key risks in the event of an adverse scenario. Observe.

All the obvious and most important risks to the financial system are conveniently laid out for anyone to see via these DFAST summaries. I’ve highlighted what I think are the 5 most critical risks to the system. “Country” and “Credit” are what I spent a lot of time on in the last and current post, but the “Model” risk is interesting to see.

All these derivatives, the swaps, the repos, etc.; they’re all evaluated with a risk-assessment model called Value-at-Risk or “VaR” for short. VaR is simply a statistical methodology for determining the risk level of an asset or portfolio. And VaR is how all the financial system institutions essentially measure the risk in their portfolios, not just the banks. The problem is that VaR works under stability until it doesn’t under instability.

VaR was utilized to assess the mortgage backed securities in the lead-up to 2008. The problem with a model is that it’s garbage in, garbage out; whether it’s a human or machine performing the assessment. The MBS valuations and thus risk assessments were off in another galaxy because the ratings agencies were saying the debt securities were AAA-rated and the models statistically showed virtually no chance of default. A biblical flood, major meteor collision, and lightning striking 20% of the world’s population would have to occur first before the AAA MBS began defaulting. Once again, we all know how that one played out.

Well we’re back at the same place as 2007 – 2008. This time, instead of housing, the name of the game is sovereign debts via the central banks and the financial institutions and corporations keeping the system propped up via debt issuance and bilateral/trilateral funding. And what models are being used to assess risk? You got it. VaR! Yarrrrr!

You may be thinking, “No way. There’s no way all these players still use the same or similar models to assess the risks of all these derivatives within their portfolios.”

Ok. Have a look at what S&P peddles. Oh wow, it’s a shiny automated VaR model to assess credit risk. And you get a nice little whitepaper to go with it to explain why you need their particular tool.

So where is all this information on derivatives? In the same places as always. The quarterly and annual reports of the publicly held players and the US Office of the Comptroller of the Currency puts out a quarterly update on bank trading and derivative activities. It’s how I obtained some of the information for this post. Have a look.

What we haven’t seen a significant amount put into operation yet is credit default swaps (“CDS”). Not only do they have the negative connotation from 2008 but players are fearful to be a counterparty in one of those transactions. As the central banks continue to flood the world with liquidity, players will begin to get greedy and believe they can structure CDS to take advantage of the next crash.

I suspect this next crash will alter the financial system and environment permanently, in light of that, entities are not going to be made whole for their CDS exposure like in 2008. That would be politically untenable and I’m not so sure that even the politicians would sign off on another flaying of the tax-paying public.

The reason you should care so much about this component of the financial system is because of the risk it introduces to the world economy and markets. Not only are the models flawed in assessing the risk in all these financial instruments, but the counterparty risk in all these derivatives are the true danger. Because of the inter-connectivity of the world’s financial institutions. It’s only going to take one. One major bank or one major insurance company. Just one to begin the domino process.

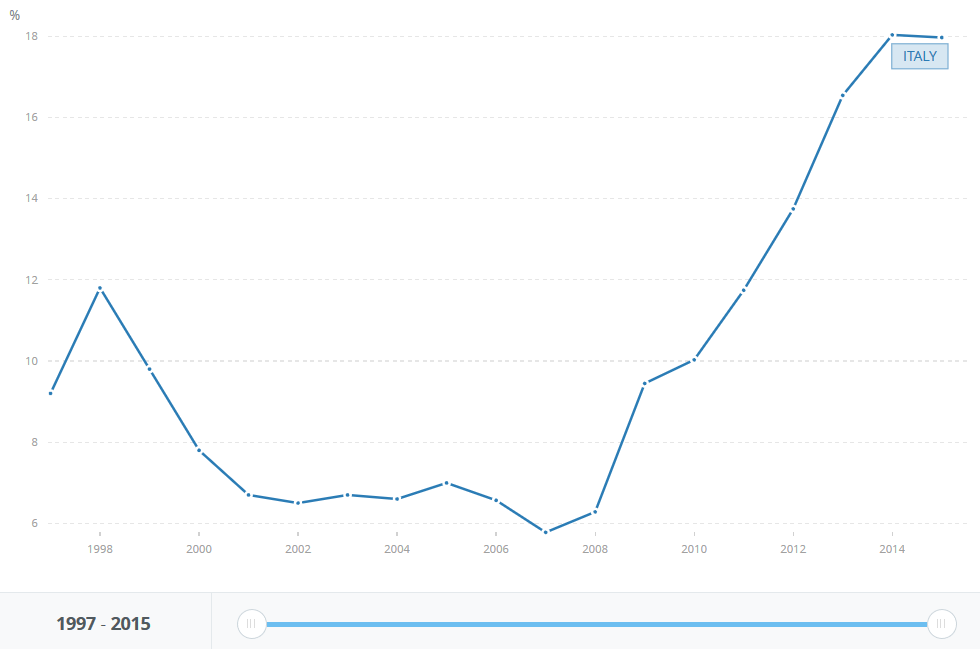

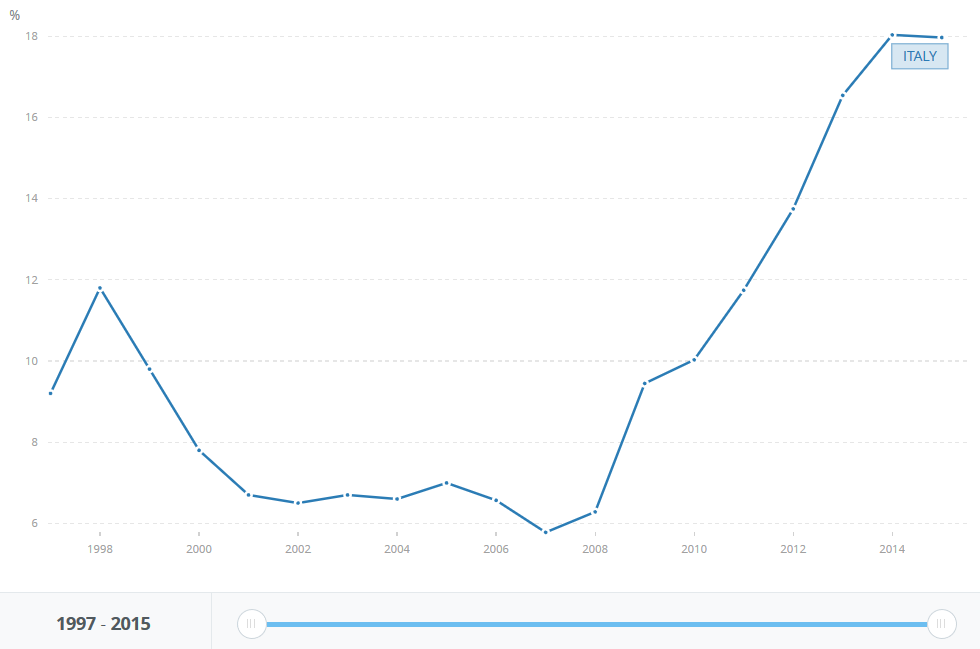

So what does that process look like? Let’s look at a feasible but extreme scenario. Italian debt as a percentage of it’s GDP is out of control. Even worse, nonperforming loans (“NPL”) i.e. bad debt within Italian debt instruments are at Depression-like percentages. Observe the following chart of Italian banking NPL through 2015 from the World Bank.

It’s clearly a problem. Now let’s say Deutsche Bank is woefully exposed to this nonperfoming debt in Italy. All it would take is a trigger like a major accounting fraud is discovered at Citigroup while derivative instruments begin crashing at Deustche and the counterparty massacre begins.

While this happens and to help allay fear, let’s say Japan and the ECB simultaneously co-announce deep cuts in their central bank interest rates of an additional -1.5% each. At the same time, the ECB announces it is going to buy 10% of all European companies with market caps over $10B. Additionally, the Netherlands announces their exit from the EU. You think fear might start rising?

Let’s add another fear factor to the scenario, Japan announces it’s going to spend $1 trillion USD on infrastructure and technology development to create jobs but simultaneously announce a $27,000 USD annual living wage. Economists call this “helicopter money” and it’s the last blank bullet Western central banks possess to stimulate animal spirits.

The scenario is extreme, but the world’s markets are dancing on a razor’s edge. Do you see why gold sounds so sound? Do you see why some exposure to precious metals could possibly help carry portfolios through the next crash? Millennia of monetary utility. Zero counterparty risk. Accepted value around the world by all people. Doesn’t sound so crazy to have exposure to the asset class, does it?

It’s just about quitting time so let’s address the two most important aspects of even knowing or sharing this information. How is it actionable and in what kind of timeframe?

Well if you’ve read any of my material over the years, you should have a pretty good idea of how I think it’s actionable. Increase cash levels. Increase precious metals exposure via the physical metal and intelligent allocations into precious metals stocks. For the latter, see the J-perp portfolio. It’s a basket of junior players that in 2016 is outperforming virtually every index and hedge fund known to man.

Begin to pare back winning positions that are leveling off. Going to cash means liquidating where appropriate in order to raise the cash. Many of the world’s best value investors have started that process some time ago.

As for timeframe, I’m more convinced than ever that sometime in 2017 is when it all begins. By begins, I mean the wobbling. Like a top slowing its spin and starting to topple. We may not see an outright initiation of a crash, but I’m confident that serious wobbling will begin. I already believe that the action at the end of 2015 and beginning of 2016 was the start of everything. That period of volatility was the waking up of the bear and the starting point for the last-gasp melt-up in markets around the world; the final blow off for profit grabbers.

Bear in mind that central banks control everything now. Sentiment and liquidity via free market operations are a thing of the past…for now. Which means that through their actions, many players believe that the universal bull market can continue for years.

I believe this to be flawed thinking. When confidence takes its leave, there’s no amount of money that can be thrown at the issue. There’s no amount of negative rates that can spur true economic development, because animal spirits will be neutralized by fear. Banks and sovereign wealth funds will be monetizing even more ludicrous amounts of varying asset classes. You thought it was crazy for central banks to start buying stocks and corporate debt? Just wait. Desperation will breed decisions that will go down in history.

It’s a fine line between pessimism and realism. I’ve shared enough of both in this post and the last. You’ve gotten useful charts. I’ve provided what I think are some important points about how the financial system truly works. Now it’s up to you to make key decisions for your own portfolios, because when the fun does stop, the amount of leveraged liquidity wending its way through the system will hasten a cataclysmic financial event.

All that being said, let’s ride the final melt-up for all that it’s worth and try to get paid.

I’ll leave readers with one final quote to sum up my thoughts on the complexity of the financial system. It’s a pithy little ditty by a recognized genius and one of history’s greatest brains, Leonardo da Vinci.

“Simplicity is the ultimate sophistication.” Here, Here.

")

")

")

")

![clip_image001[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0016.png "clip_image001[6]")

![clip_image002[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0026.png "clip_image002[6]")

![clip_image003[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0036.png "clip_image003[6]")

![clip_image004[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0046.png "clip_image004[6]")

![clip_image005[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0056.png "clip_image005[6]")

![clip_image006[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0066.png "clip_image006[6]")

![clip_image007[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0076.png "clip_image007[6]")

![clip_image008[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0086.png "clip_image008[6]")

![clip_image009[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0096.png "clip_image009[6]")

![clip_image011[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0116.jpg "clip_image011[6]")

![clip_image013[6]](https://marginrich.com/wp-content/uploads/2016/01/clip_image0136.jpg "clip_image013[6]")